LinkUp Forecasting Robust Job Gains of 290,000 for May

Jun. 05, 2019

Source: Toby Dayton, LinkUp CEO

Occasionally over the years, it’s been the case that as I am working on our non-farm payroll forecast, I’ll hear a song that is extremely relevant to the current employment situation.

Occasionally over the years, it’s been the case that as I am working on our non-farm payroll forecast, I’ll hear a song that is extremely relevant to the current employment situation. It happened again this month when I recently heard Marvin Gaye’s Inner City Blues (Make Me Wanna Holler). Not only a great song, it’s as relevant today as it was in 1971.

Between income inequality, tax cuts for the wealthy, stagnant real-wages, war (if one includes the present threat of it in the case of Iran), social injustice, racism, police brutality, and the national and even global panic caused by a lunatic in the White House, the lyrics couldn’t be more applicable to society today as they were 50 years ago. Unfortunately, hollering doesn’t even begin to capture the emotion stemming from the dysfunction of the country these days.

And that 50-year horizon is depressingly appropriate these days given that of all the statistics around the labor market over the past 10 years, and particularly in the past 5 years as unemployment has steadily dropped, the most insane fact is that average hourly earnings for production and nonsupervisory workers in the U.S. have not increased one nickel since 1972.

I would argue that if one were forced to name the single most relevant statistic that captures all the forces driving our society over the past 5 decades, that would be the one. Nothing so potently encapsulates both the cause and/or result of essentially every major force impacting our society: Social, racial, and socio-economic inequality, dysfunctional democracy, broken capitalism, polarization, insane politics, urbanization, globalization, immigration, education, modernization and technology, demographics, human rights, labor relations, public policy, social policy, and on and on and on.

In the past 15 years or so, these major tectonic forces have come into particularly sharp relief with The Great Recession, the jobless recovery, and, more recently, what one might call the Raiseless Expansion. Although there have been some modest hints of wage inflation very recently, the persistent absence of wage inflation has been an extremely perplexing phenomena. Some would even say distressing – The Fed Chair has called weak inflation ‘one of the major challenges of our time.’ And a New York Times article entitled ‘The Economy is Strong and Inflation is Low. That’s What Worries the Fed‘ points out, a healthy bit of modest inflation is key to wages because it allows wages to climb without impairing profits. This is why Janet Yellen described inflation as the lubricant on the wheels of the labor market.

Over the past few years, as inflation in general and wage inflation in particular have remained essentially dormant, people have pointed to dozens of causes such as technology, globalization, automation, the ‘Fissured Workplace’, the demise of unions, increased concentration within industries which reduces competition for labor, stagnant productivity, excessive slack in the labor market, etc. There is sound logic behind most, if not all, of these arguments and the truth is undoubtedly some combination of them all.

Additionally, many have made the case that inflation and wage inflation exist but are simply hidden because they are being poorly measured or cannot be measured at all in today’s increasingly complex economy. And while some of those arguments also have some merit, the award for the most baseless, cynical, and offensive argument goes to Phil Gramm and John Early who, in a recent WSJ editorial entitled ‘The Myth of Wage Stagnation,‘ attempt to pacify anyone enraged about stagnant wages, income inequality, or social immobility by critiquing the government’s current methodology for measuring inflation and haranguing people to stop obsessing about their paycheck and focus instead on their HD TVs and the abundance of ‘out-of-season’ fruit available in the supermarket. I’d be hard pressed to imagine a more abhorrent ‘Let them eat cake’ moment anywhere in my lifetime.

Turning back to the real world, arguably the two major contributing factors to low wage growth are low productivity and persistent slack in the labor market.

Regarding the former, in a WSJ editorial entitled ‘Mind the Prodcutivity Gap to Reduce Inequality’ by Edward Lazear makes the case that rising productivity among the top wage earners in the country is the reason for significantly faster wage growth among that group. “Wage growth for the median worker has stalled at about 0.5% a year in the U.S. The likely explanation is that changes in trade and technology have raised the productivity of highly trained, highly educated workers relative to the less skilled. Wages tend to move with productivity, so that if differences in worker productivity grow, wage differences will also grow.”

Lazear goes on to point out that “the median German earns 55% of what the 90th-percentile German worker earns, while the median American worker earns only 41% of what the 90th-percentile American worker earns” because “Germany has a system that relies heavily on vocational training. Those who don’t go to college obtain market-oriented skills during their high-school years. That training appears to boost their productivity relative to their American counterparts. Average productivity in the U.S. is high, but there are many Americans whose productivity is low because the U.S. educational system doesn’t develop real labor skills for those who don’t go on to college. German vocationally trained workers, many in services, do better relative to the average than do American high-school graduates, let alone American high-school dropouts.”

A recent study from Brookings makes a related point in comparing wage gains in red versus blue counties in the U.S. The study found that while job growth is accelerating faster of late in red counties, “that growth hasn’t translated into pay gains. After inflation, average weekly earnings in Trump country fell at a 0.3 percent annual rate, down from 0.6 percent growth in Obama’s final years. Workers in Democratic-leaning areas did better, with pay rising at a 0.1 percent rate, down from 0.9 percent annual gains during Obama’s last two years.”

The study noted that, “Red America jobs also are more vulnerable. Many are the types of physical and routine labor that is especially susceptible to automation and outsourcing abroad. And industries such as mining, oil and gas and construction that are adding jobs in Red counties would be among the first hit in a recession. American agriculture, already hit by five years of decline in farm income, is being squeezed by Trump’s trade conflicts and the sector’s financial pain.”

More broadly speaking, the insecurity and frustration of the average American worker is highlighted in a NYT editorial entitled ‘Strong Economy, Worried Americans’ by Jacob Hacker. In explaining why 60% of Americans feel the economy only helps ‘those in power,’ Hacker argues that as a society, we have shifted massive amounts of risk to employees. The elements of what he calls “The Great Risk Shift” include things like outsourcing, off-shoring, part-time work, the gig economy, deregulation, volatile shift schedules, inadequate child care, anti-union policies, employer-driven health insurance, a dearth of training, rising tuition costs, and horrifically inadequate public education, to name just a few. All of these factors have given employers a massive amount of power and leverage relative to workers which has allowed them to keep wages exceedingly low even while unemployment has plummeted and the labor market has tightened dramatically in the past 10 years.

Adding to those forces is the fact that many business owners simply refuse to raise wages despite an increasingly acute supply/demand imbalance. Whether it is based on logic, philosophy, emotion, or some other factor(s), a huge number of employers will only raise labor costs as the absolute last resort (if they do it at all). As the Minneapolis Star Tribune points out after interviewing Minneapolis Fed President Neel Kashkari:

“Since his start at the Minneapolis Fed, Kashkari has traveled the six states — from Montana to Michigan — in which it oversees banking and asked business executives for their read on the economy. He frequently heard complaints about worker shortages but, when he asked if they were raising wages, executives said they didn’t want to do that.

He realized business owners and executives look at wages differently from other costs. Partly that’s because when wages rise, they rise permanently since it’s virtually impossible for an employer to cut workers’ pay. But Kashkari said he also believes emotions are involved.

“If the price of steel or oil or corn, or any input into their business, goes up, they say ‘Oh well the market price went up, I have to pay it.’ But if they’re trying to hire workers, they only want to pay wages that they’re used to paying. And if the workers are not available, they say ‘Oh my gosh there’s a worker shortage,’ ”Kashkari said. “No, the price just went up.”

Companies like Marlin Steel Wire Products will spend $2 million on robots before they’ll raise wages (or license an applicant tracking system and enter the 21st century). To be clear, investing in robotics is perfectly reasonable business decision, but irrational resistance to raising wages defies logic. And in any event, technology, automation, and robotics are only adding to the already precarious position of the average worker. Through this recovery, as companies find it increasingly difficult to fill open positions and technological advancements continue to accelerate, companies are increasingly turning to robots to get work done while lowering costs and increasing efficiency and productivity. And we’ve seen nothing compared to the disruption that’s coming with autonomous vehicles, full-scale AI, and accelerating adoption at scale across the economy.

The second major contributing factor that has absolutely been instrumental in the absence of meaningful wage growth in this recovery has been the persistently surprising amount of slack in the labor market. As the labor market has tightened and employers have belatedly and begrudgingly raised wages one penny at a time, more and more people have entered the workforce. While that makes sense and isn’t all that surprising in hindsight, the economy has thawed pockets of workers such as felons, retirees, disabled workers, and opioid addicts that had previously been believed to be permanently frozen out the labor force. As a March WSJ article entitled ‘Labor Force Rate Defies Declines – For Now’ points out:

“Since bottoming out in September 2015, the share of the population aged 16 and over working or looking for work has stabilized around 63%, cutting against an extended decline tracing back to 2001. Many economists had been predicting continued declines in the rate. In just the past six months, the number of people outside the labor force has fallen by 1 million, the largest such decline on record.

“The performance of labor-force participation over the last three or four years has been an upside surprise that most people didn’t see coming,” said Fed Chairman Jerome Powell at a news conference this week.

As Kashkari points out in a WSJ op-ed and the same Star Tribune article, there are still people on the sidelines who are emerging to take jobs as wages rise. If the participation rate of working-age workers, defined as those ages 25-54, were as strong today as it were in 2000, another 2.3 million Americans would be working, he said. Economists debate reasons for the decline of workforce participation in the U.S. Theories vary — the effects of automation, the opioid crisis, technical-skills gap are considered — but these ideas don’t satisfy Kashkari. “There’s no good explanation for why it should be lower,” he said. And if it shouldn’t be lower, he said, more people will continue to take jobs as wages rise. He noted that the April jobs report showed that more than 70% of people who were hired indicated that they weren’t looking for jobs in March.

Given the continued evidence of persistent slack in the labor market, Kashkari argues that:

The Fed’s rate-setting policymakers and other economic observers should pay more attention to price signals for labor rather than the unemployment rate. “We are seeing wage growth pick up. Clearly the labor market is tightening,” he said. “But is the market really tight yet? The answer is no.”

For the Fed, he said, that means it’s not time to raise interest rates.

“I’m not dogmatic about this. If wage growth picks up a lot, I would say ‘Hey, it looks like we’re there,’ ”Kashkari said. “But until that happens, we’ve got to let this economy continue to strengthen.”

On the economic front, the bond market indicates that investors are getting increasingly nervous about more trade wars (with Mexico?!), jittery businesses, the global economy, and slowing growth in the U.S. Others point to positive signs such as rising productivity and the fact that 3% GDP growth might be sustainable for 3-5 more years.

On the job market front, the economy added 263,000 jobs in April, the 103rd straight month of positive job gains, while the unemployment rate dropped to 3.6%. There are now more job openings than unemployed people (some people’s definition of full employment) and average hourly earnings have risen 3.2% in the past 12 months. Additionally, there are 4.7 million people in part-time jobs who want full-time work and another 1.2 million people who have been looking for work for 6 or more months.

With all the conflicting signals, it’s brutally difficult to know where we’re headed. And as Kashkari points out, it’s never been more important to get it right. “The Federal Reserve needs to read the labor market correctly to determine how to achieve its dual mandate of stable prices and maximum employment. Because monetary policy operates with a lag, it is critical to know ahead of time if the labor market will approach maximum employment or if inflation will exceed the target rate. Misinterpreting the indicators can lead directly to bad policy that hurts the economy.”

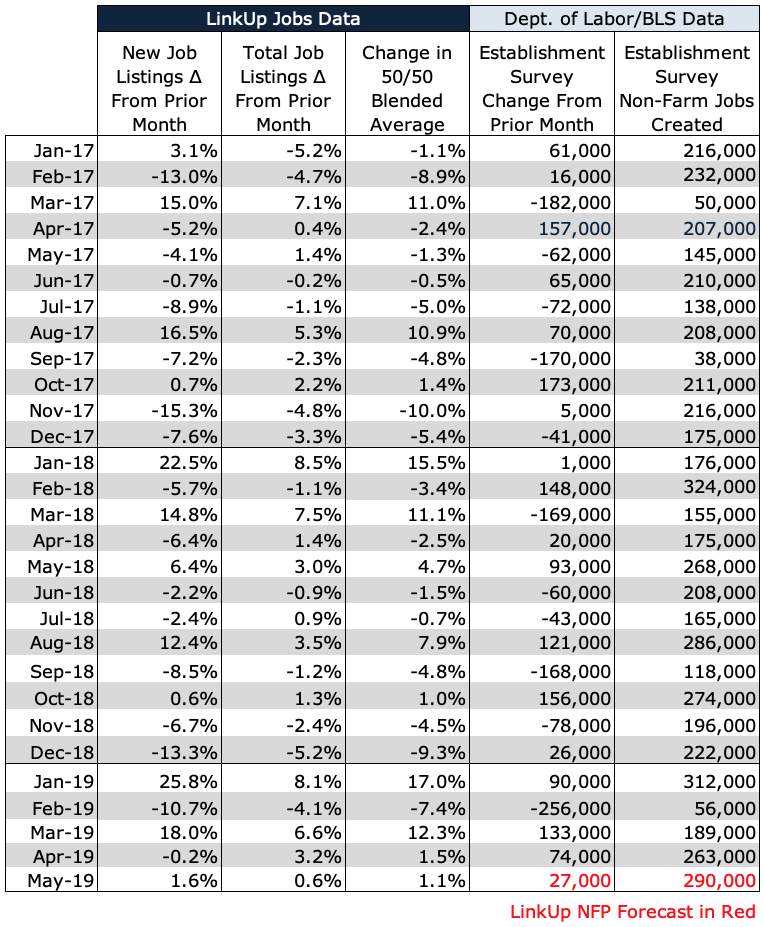

Not surprisingly, we’re strongly of the opinion that LinkUp’s job market data is the best place in the world to read the labor market correctly. And based on our data from last month, we are forecasting a net gain of 290,000 jobs for Friday’s jobs report for May.

Looking at our paired-month data for May, where we compare job openings in April and May for companies that were actively hiring in both months, new and total job openings rose 2% and 1% respectively, with gains across a majority of states.

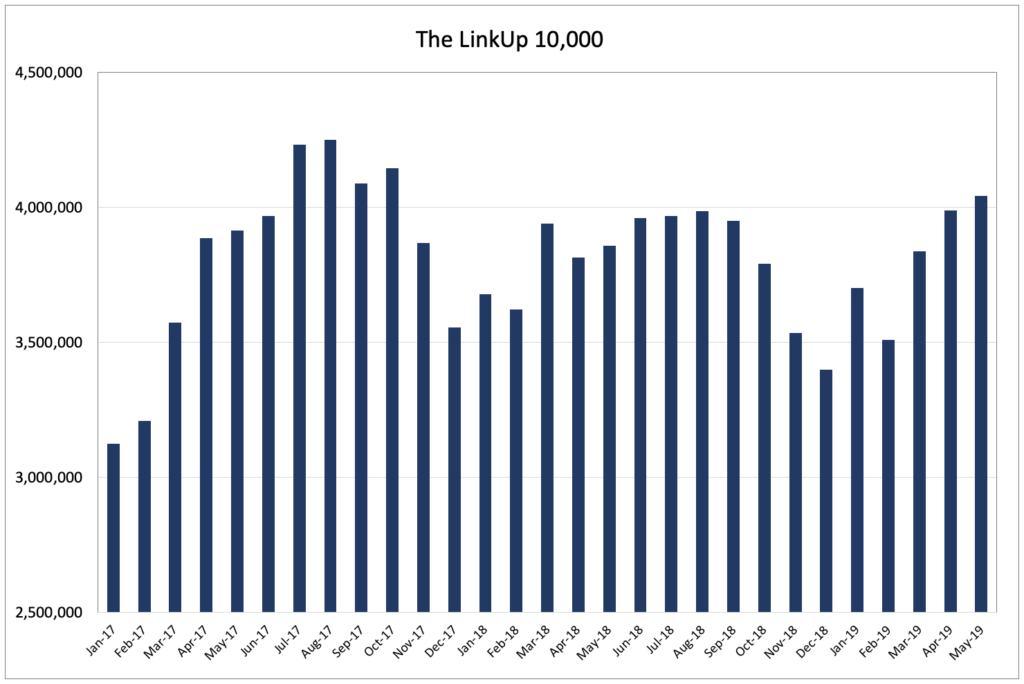

The LinkUp 10,000, which measures labor demand on a daily and monthly basis for the 10,000 employers in LinkUp’s job search engine with the most job openings, rose 1.3% in May to just over 4 million job openings.

And looking at LinkUp’s entire job openings dataset for the U.S., total jobs rose 0.9%, new jobs fell 8.9%, and removed jobs rose 9.3%. The slight rise in total job openings is definitely a positive signal but the drop in new job openings is potentially a warning sign for job gains in June/July. And because companies remove job openings from their corporate websites when they are filled, the sharp drop in job listings in May is a very strong signal that points to solid job gains during the month.

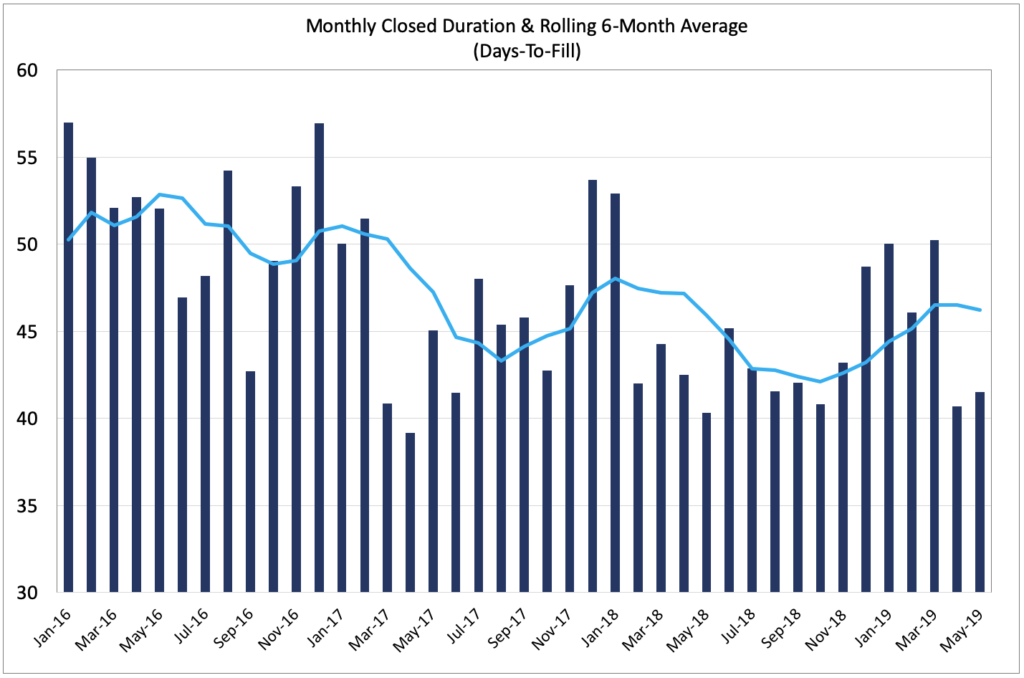

Our Job Duration metric, which measures the average number of days that jobs are listed before they are filled – essentially a hiring velocity indicator, rose slightly to 41.5 days, still very low by historical levels and indicative of very high hiring velocity.

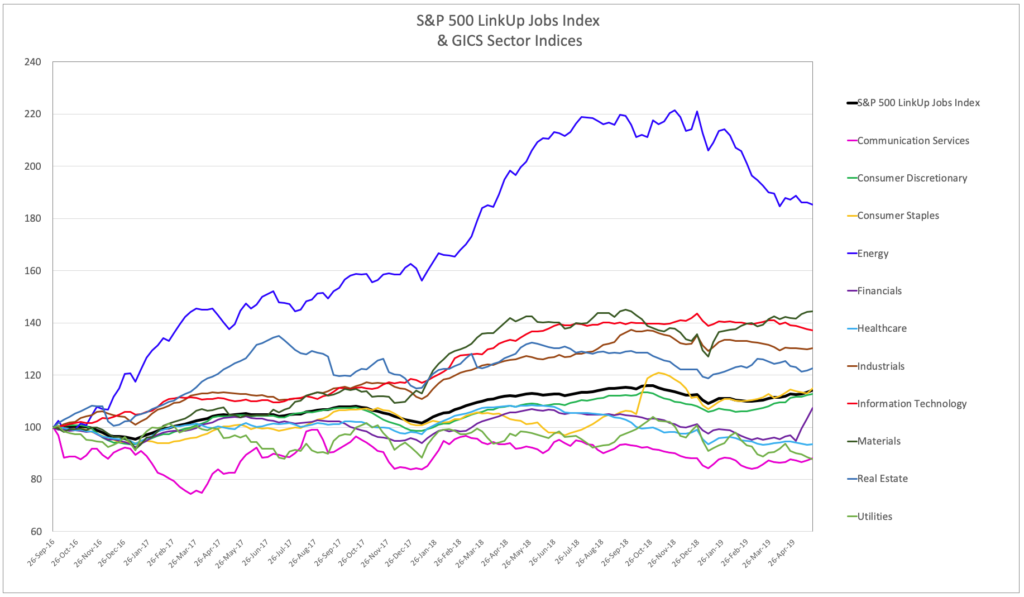

And lastly, the S&P 500 LinkUp Jobs Index, which measures weekly labor demand for the S&P 500, rose 0.8% from the prior week for the week ending May 20th. That was up 1.5% from 4 weeks prior.

Of particular note at a GICS sector level, labor demand among financials rose 4% from the prior week.

So based on our award-winning jobs data for May (which, by the way, is sourced entirely from company websites around the world every day which makes it the largest and most accurate dataset of jobs available in the market), we are forecasting a net gains of 290,000 jobs in May.

But then again, as Marvin Gaye sings in Inner City Blues, “God knows where we are heading.” Maybe we’ll find out Friday.

Insights:

Related insights and resources

Blog

02.04.2021

U.S. Labor Demand Is Growing But January Jobs Numbers Will Disappoint Tomorrow